Posted on

SALT deductions. Sounds like something that your doctor recommends when you go for your annual physical – which I know we all do every year without exception. However, that’s the NaCl type of salt and not what we’re talking about here. So, what is this deduction you might ask. It’s the amount you can deduct from your federal income due to State And Local Taxes you have paid, commonly referred to as SALT.

With the new tax laws for 2018, we have seen some changes to the SALT deductions that you are allowed to take. But before we get into that let’s cover some of the basics. For these purposes, the SALT deduction consists of 3 different types of taxes; real estate/property tax, state and local income tax, and sales tax. You might be asking yourself why you have not heard of these deductions since you’ve certainly encountered these taxes when you’ve filed your returns every year. Well, for most people, their itemized deductions (where SALT would be included) are less than the standard deduction so they never have to think about it. This deduction is usually reserved for those in high tax states or those who pay a lot in property taxes because the SALT deduction is a combination of their property tax and EITHER their income tax OR their sales tax. To clarify that last point, the SALT deduction requires you to make a choice between deducting state income tax or sales tax. In the majority of cases, the filer will use their state and local income taxes. However, if you live in a state with no state income tax or you had a year with a lot of big purchases, deducting sales tax could be the right decision for you.

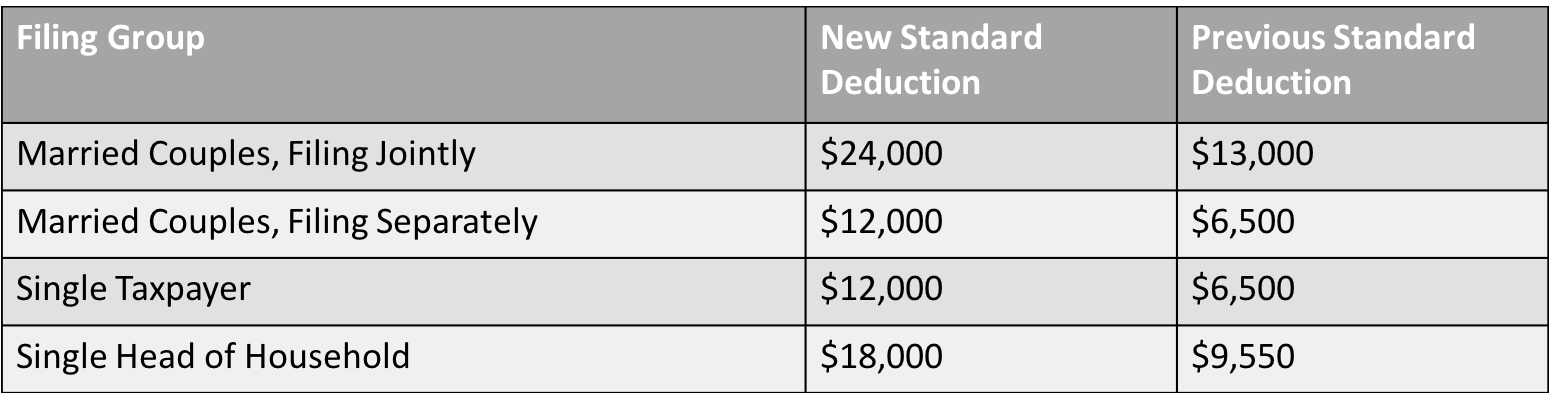

Now that we know what the SALT deduction is, let’s take a look at what was affected by the changes that were made in 2018. Very simply, there are 2 major factors to think about when considering how an update to the SALT deductions affects people. The first, and likely the largest, is that there is now a cap on the amount of money you can deduct related to SALT. This used to be unlimited, but it has now (2018) been changed to a maximum of $10,000. The second factor is the standard deduction because, as we said above, most people will not exceed the standard deduction when they sum all of their eligible itemized deductions. This is important because the goal is to have the largest deduction possible. The standard deduction changes by group:

To summarize, we can now itemize a maximum of $10,000 in SALT on our deduction, but we also have a higher standard deduction available. How these changes ultimately affect us is really a case by case consideration. Some people who have itemized in the past will net out even by switching to a larger standard deduction, but some people will be highly affected, namely high earners in high tax states. Let’s take a look at our friend Tony from our blog about tracking your days (which you can read here) for an example.

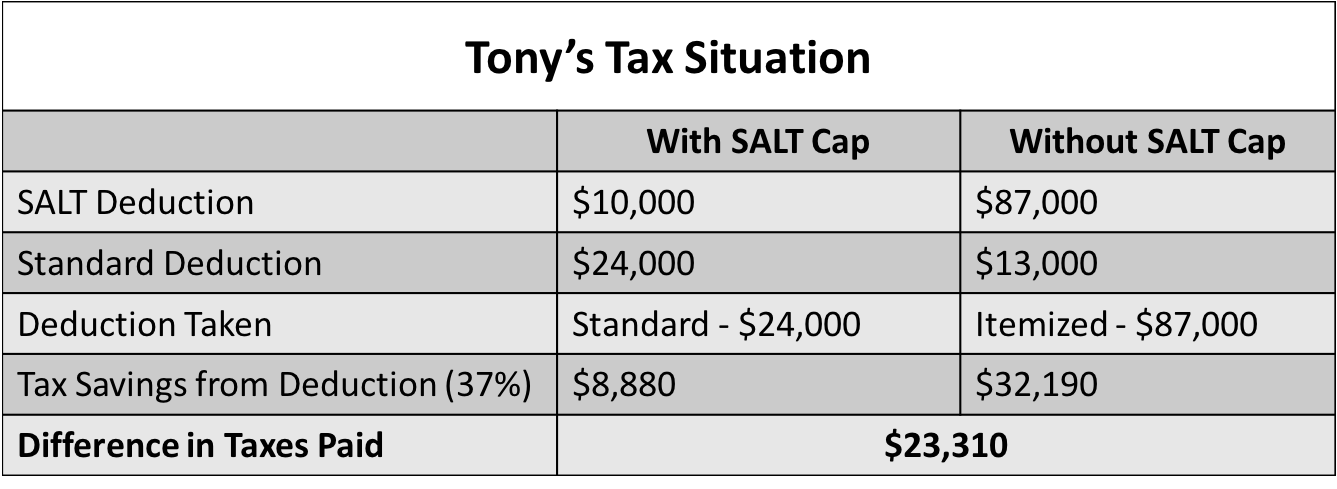

Let’s quickly recap Tony’s situation - and we’ll summarize in a chart below in case this gets confusing. He makes $1MM per year as an exec at an online retailer (again, well done Tony). He is domiciled in Florida so he can save on those state income taxes, but he owns a second home in New York. Not mentioned before but just so you know, his property taxes for both homes total $20,000. And, for this example, let's say that Tony messed up really badly and forgot to track his days and ended up being a statutory resident of New York by spending too much time there (come on Tony, all you had to do was check your TaxBird notifications!). As a New Yorker, Tony pays approximately $67,000 in New York income taxes. Before the cap, Tony would have been able to deduct $87,000 (New York income tax and his property taxes) plus any additional itemized deductions from his federal income. Now, he can only deduct $10,000 of the $87,000. To keep it simple, let's imagine Tony had no other itemized deductions. So, with his itemized deduction at just $10,000, he’s better off using the $24,000 standard deduction for married couples filing jointly. This means Tony’s change in taxable federal income is $63,000, the difference between the new standard deduction and old uncapped SALT deduction. That $63,000 would be taxed at the highest federal rate of 37% meaning Tony pays an extra $23,310 in federal taxes.

Now Tony has both salt and SALT to thank for messing with his blood pressure.

The numbers and example in this blog are meant to be a very simple guide to highlight the changes in SALT deductions. To better understand if these changes affect your situation, you should consult with your tax professional.

Sign up for email updates, notifications on new blog posts, and local events.

Subscribe