Posted on

Welcome back to our two-part blog on how to save on your taxes. If you read part one, you know that Tony - my always entertaining and often in trouble friend - got me thinking about what I can do to save on my taxes this year. He had told me a few “tricks” he used to cut down his tax bill last year. Tricks that I’d be curious (and a bit afraid) to have legally reviewed. So, with legality in mind, I did some research to see what can be done to save on my taxes.

The techniques that I found can be broken down into two major categories – decreasing your adjusted gross income and increasing your deductions and tax credits. Read part one for some tips to decrease your above the line income (you can find it here). You’ll definitely want to check it out, but you don’t need to read part one prior to what we’ll cover here, so you can save that for later. On this blog, we’ll take a look at standard vs. itemized deductions and tax credits.

Let’s start with the deductions. First thing to know - what’s the difference between the two options: standard deduction and itemized deduction; and how do I know which is right for me? The standard deduction is what you’re entitled to deduct from your income as set by the IRS for your filing status. Nearly every tax payer is eligible to take this deduction and there is nothing to calculate to figure out what it is. According to irs.gov, the exceptions to the standard deduction are:

-

A married individual filing separately from their spouse and the spouse is taking the itemized deduction

-

An individual who files a tax return for a period less than 12 months due to changes in their annual accounting period

-

An individual who was a nonresident alien (NRA) or a dual-status alien during the year. There is an exception for a NRA who is married to a U.S. citizen or resident alien at the end of the year and choose to be treated as a resident for tax purposes – those individuals can take the standard deduction.

-

An estate or trust, common trust fund, or partnership.

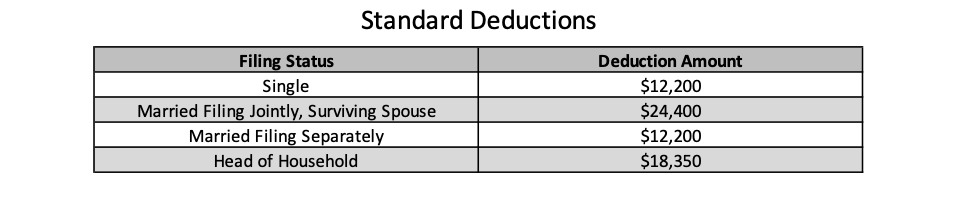

The standard deduction amount varies depending on your income, age, whether or not you are blind, and filing status. It also changes each year - see below for the standard deduction by filing group for 2019.

Also, for 2019, the additional standard deduction amount for the aged or the blind is $1,300. The additional standard deduction amount increases to $1,650 for unmarried taxpayers.

Itemized deductions, on the other hand, are related to your tax-deductible expenses during the year. These expenses can come from medical bills, state and local taxes (SALT), home mortgage interest, charitable donations, and others.

But how do you choose which deduction type is right? Well, turns out it’s actually pretty simple. If the total of your allowable itemized deductions are greater than the amount of your standard deduction or if you can't use the standard deduction, you’ll want to itemize. Easy right? The complexity comes from figuring out your itemized deductions so let’s cover the most common ones, so you know what to include in your consideration.

-

Medical And Dental Expenses

-

Medical and dental expenses that exceed 7.5% of your adjusted gross income may be deductible. This includes expenses for yourself, your spouse, or your dependents. Find out more here.

-

-

Deductible Taxes

-

There are four types of deductible taxes:

-

State, local, and foreign income tax

-

State and local general sales tax

-

State and local real estate tax

-

State and local personal property taxes

-

-

As of 2018, the the state and local taxes that you can deduct are capped at $10,000.

-

Find out more here.

-

-

Home Mortgage Points

-

As long as you meet several requirements, you should be able to deduct the prepaid interest as home mortgage interest. Read the details and requirements here.

-

-

Interest Expense

-

There are two types of interest available to be claimed as itemized deductions – investment interest and qualified mortgage interest. Other interest expenses might be able to be claimed elsewhere on your return but these two can be used toward itemized deductibles. Find out more here.

-

-

Charitable Contributions

-

As long as the donation is provided to a qualified organization, the contribution is deductible. If you receive a benefit from the donation, you may only deduct the portion that exceeds the value of the benefit. For more information on qualified charities and details on how to deduct, go here.

-

-

Business Use of Home or Car

-

If you use your home or car for business purposes, you might be able to deduct expenses related to either or both of them. If you have an area of your home dedicated to a business use, you can find the details for the deductible here. If you use a vehicle for business, even if it’s not full time, you can find information on the deduction here.

-

-

Business Travel Expenses

-

If you need to travel outside of the general area where you usually work, the expenses related to that travel can be deductible. The expenses include air/bus/train/car travel, transportation while in the destination city, shipping of baggage or materials, meals, hotels, among some other things. Find out more info here.

-

-

Work-Related Education Expenses

-

If you have educational expenses related to maintaining/improving your job skills or you need education related to a requirement by law, those are deductible. The deductible expenses from education include tuition, books, supplies, lab fees, some transportation costs, and a few other miscellaneous expenses. Find out more here.

-

-

Casualty, Disaster, and Theft Losses

-

If you have casualty or theft losses relating to your home, household items, or vehicles due to a federally declared disaster area, you can include these on your itemized deductions. If the losses were covered by insurance, you can only claim the amount of the loss less any reimbursement or expected reimbursement. Find out more here.

-

As I said above, you should figure out your deduction for each of these areas and total them up. If the sum of your deductions exceeds the standard deduction, you should itemize your deductions on your returns.

Now for tax credits. If you qualify for any tax credits, they are a great way to offset your tax bill because a tax credit decreases your taxes, dollar for dollar. What’s that mean exactly? As an example, a $1,000 tax credit will decrease the amount you owe by the full $1,000, unlike a deduction which helps decrease the total income that will be taxed. There are two types of tax credits – refundable and nonrefundable. A refundable tax credit can always be taken in the full qualifying amount, even if it’s more than what you owe for the year…which would get you a refund. Clever naming, right? Nonrefundable credits forfeit any amount from the credit that is greater than what you owe. The credits are broken into 5 main categories:

-

Family and Dependent Credits

-

Earned Income Tax Credit

-

Child and Dependent Care Credit

-

Adoption Credit

-

Child Tax Credit

-

Credit for the Elderly or Disabled

-

-

Income and Savings Credits

-

Saver’s Credit

-

Foreign Tax Credit

-

Excess Social Security and RRTA Tax Withheld

-

Credit for Tax on Undisputed Capital Gain

-

Nonrefundable Credit for Prior Year Minimum Tax

-

Credit to Holders of Tax Credit Bonds

-

-

Homeowner Credits

-

Residential Energy Efficient Property Credit

-

Nonbusiness Energy Property Credit

-

Low Income Housing Credit

-

-

Health Care Credits

-

Premium Tax Credit

-

Health Coverage Tax Credit

-

-

Education Credits

-

American Opportunity Credit and Lifetime Learning Credit

-

If any of these credits look like they might apply to you, you can find more detailed information (and usually quizzes to help understand if you qualify) on irs.gov here.

My goal for this two-part blog was to build your awareness of some tax-saving possibilities. Make sure your accountant or tax preparation software helps you navigate any area that might apply to you. I hope this helps put you in the best possible tax situation for 2019!

Questions, comments, feedback? jared@ware2now.com

Sources, links, additional reading:

https://www.irs.gov/taxtopics/tc500

https://www.irs.gov/credits-deductions-for-individuals

https://www.nerdwallet.com/blog/taxes/what-tax-credits-can-i-qualify-for/

Sign up for email updates, notifications on new blog posts, and local events.

Subscribe